FedEx (FDX) is known for making constant share buybacks to achieve its EPS targets. It made share repurchases in the last quarter, and it can continue to do so, since it still has to buyback 7.4 million out of 10.0 million shares as per the share repurchase program started in March 2013. A big question is whether the company actually needs to repurchase shares to achieve its EPS target.

Apart from what lies ahead with share repurchase, another area of interest is the company’s FedEx Ground and FedEx SmartPost segments, which are its shipping divisions. These sectors cumulatively witnessed the highest operating margin of 17% amongst all FedEx’s operating segments in the last quarter. With a promising operating margin, can both the segments drive FedEx’s topline?

Expecting a better result from most profitable segments

FedEx’s ground and smartpost segment generated revenue of $2.73 billion in the recent quarterly results, witnessing an 11% rise year over year. The major reason behind this revenue growth was the continued growth in home deliveries and commercial business services.

Apart from this, FedEx SmartPost individually witnessed a 26% rise year over year in its average daily volume in the last quarter results. This segment specializes in low weight and less time sensitive consumer package business. Since both are shipping services, FedEx SmartPost revenue is included in FedEx Ground.

The company expects that earnings and revenue growth will continue in the present quarter driven by FedEx Ground and FedEx SmartPost. FedEx generated around 24.5% of its total revenue from these two segments in the last quarter. FedEx mentioned that it will continue to make capital expenditures in the ground segment, and 90% of the capital expenditure allocated toward the ground segment would be to expand capacity and build new hubs.

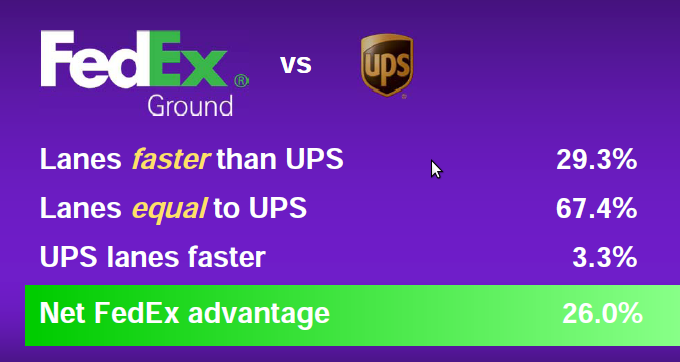

Let’s compare FedEx Ground with its biggest competitor, United Parcel Service (UPS).

Source: FedEx roadshow August, 2013

FedEx has the upper hand compared to UPS in the ground segment since it has faster lanes than UPS, offering faster transit. It also gives us an indication that FedEx has developed better infrastructure for the ground segment than UPS. In the last three years, FedEx improved the transit times by more than 50% by developing its city to city shipping lanes. We expect that FedEx will continue to develop its lanes since it allocates a good sum of money toward capital expenditure in the ground segment.

The growing e-commerce business also supplemented the topline growth for FedEx SmartPost. Online retail sales were estimated to be around $225.5 billion in 2012 in the U.S., and it is expected to reach $434.2 billion in 2017. To harness this growth, FedEx has already developed e-commerce facilities in the form of electronic shipping tools and development of its FedEx ship manager application. Such developments will also benefit the FedEx ground segment. The company expects growing online retail sales will drive the revenue for FedEx Ground since it has already noticed the impact in the average daily volume for the segment.

Let’s have a look at the average daily volume from FedEx Ground:

Source SEC Filings of the company

The average daily volume, or ADV, for FedEx Ground has been growing at an average of 2.6%. Moreover, the ADV of FedEx SmartPost is growing at an average of 7.1% over the same period. Considering a scenario where the ADV of FedEx Ground increases at the same rate for the present quarter, then the average daily volume for FedEx Ground will be 4,428,000 packages. Applying the same methodology, the average daily volume for FedEx SmartPost will be 224,100 packages.

If the revenue for the quarter increases at the same rate as the increase in ADV, then we can expect revenue of $2.81 billion for both FedEx Ground and FedEx SmartPost combined. This will lead to an increase of 3% in the segment’s revenue quarter over quarter. So according to our analysis, the segment will continue to ensure topline growth for FedEx.

Is it required to make further share repurchases to achieve the EPS target

FedEx plans to achieve an EPS growth target of 7% to 13% year over year in the present fiscal year. The company is already active in achieving this target, since it repurchased 2.82 million shares in the last quarter, which led to cash outflow of $277.76 million. This repurchase raised the EPS to $1.54 for the quarter, a 5.5% rise year over year. This share repurchase didn’t significantly increase FedEx’s EPS; without the repurchase, EPS would have been $1.53 for the quarter.

If the company completes the current repurchase program, then it will lead to a cash outflow of $870 million. Does the company really require the repurchase plan to meet its EPS guidance?

The company’s net earnings grew at an average rate of 13.38% in the last three fiscal results. Even if the company achieves half of this earnings growth, it can witness net income of $1.66 billion, resulting in an EPS of $5.25 by the end of the present fiscal without additional share repurchases. This would lead to 7.1% EPS growth by the fiscal end. So according to our analysis, the company can achieve its EPS target without making any share repurchase, but if its EPS target changes to a higher estimate, then it may require the share repurchase.

Valuation

A close analysis of FedEx and its peers, which include UPS and C.H. Robinson (CHRW).

| Company | TTM EV/Revenue | TTM EV/EBITDA | PEG Ratio (5 years) |

| FedEx | 0.79 | 6.15 | 1.24 |

| UPS | 1.68 | 29.05 | 1.73 |

| C.H. Robinson | 0.83 | 13.00 | 1.76 |

Source: Yahoo finance

FedEx is ahead of its peers regarding generation of revenue with respect to enterprise value. Moreover, from the profitability front, the company is generating the highest EBITDA with respect to enterprise value in comparison to its peers. Apart from these two indicators, FedEx’s long-term growth also seems highest when considering P/E since its PEG ratio is also the lowest. We can infer that the company may outperform since its valuation seems attractive in comparison to its peers.

Conclusion

We have considerable expectations that FedEx Ground will ensure topline growth for FedEx, and the segment will increase its share of the company’s overall revenue. If any segment reports diminishing revenue for FedEx, it can offset this with the higher revenue growth from the ground segment.

Based on our EPS estimates, we can say that company can generate enough profits to achieve its EPS target. We believe the company’s action plans are enough to ensure both topline growth and achieve its EPS growth target of 7% to 13%, so we recommend a buy for the stock.

Additional disclosure: Fusion Research is a team of equity analysts. This article was written by Shweta Dubey, one of our research analysts. We did not receive compensation for this article (other than from Seeking Alpha), and we have no business relationship with any company whose stock is mentioned in this article.